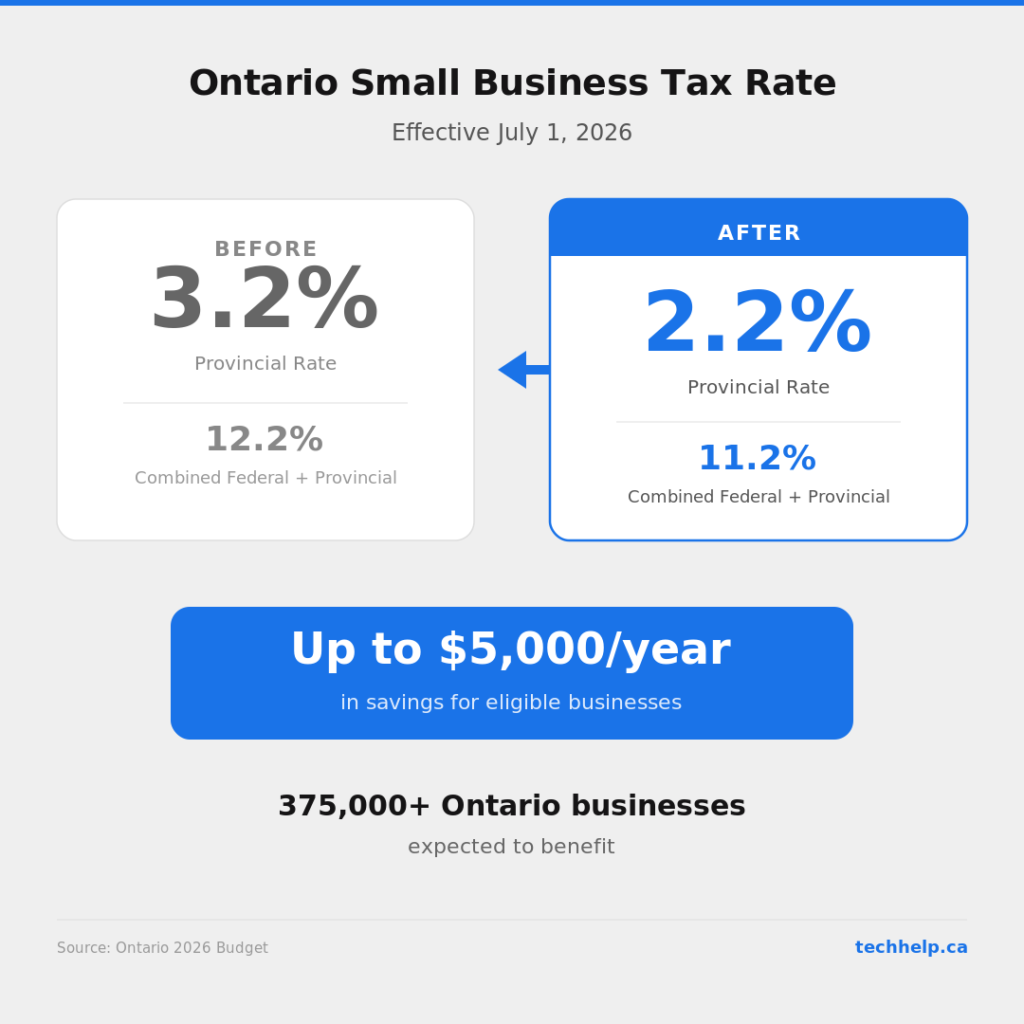

If you run an incorporated small business in Ontario, you’ve probably heard the headline: the provincial small business tax rate is dropping from 3.2% to 2.2%, effective July 1, 2026. That’s a 31% reduction, and on the full $500,000 of eligible active business income, it works out to up to $5,000 in annual savings.

More than 375,000 Ontario businesses qualify. The Canadian Federation of Independent Business called it a direct response to their top advocacy priority. And for owners feeling the weight of tariff disruptions and soft demand, any relief is welcome.

But there’s a second change buried in the same budget that most coverage glosses over. Starting January 1, 2027, Ontario is also cutting the non-eligible dividend tax credit, which means you’ll pay more personal tax when you pull those corporate savings out as dividends. Whether this rate cut actually puts more money in your pocket depends on your structure, your compensation strategy, and what you do in the next six months.

Ontario’s 2026 budget, titled A Plan to Protect Ontario, included a permanent reduction to the province’s small business corporate income tax (CIT) rate. For eligible corporations, the levy on the first $500,000 of active business income falls by a full percentage point.

When you combine that with the federal small business rate of 9%, the total corporate tax rate on qualifying income drops from 12.2% to 11.2%. The Ontario government projects $1.1 billion in total tax relief over the next three years.

This isn’t a temporary pandemic-era credit or a one-year incentive. It’s a permanent rate reduction baked into the tax code going forward.

Do you qualify?

The reduced rate applies specifically to Canadian-Controlled Private Corporations (CCPCs). To access it, your corporation needs to meet a few conditions.

First, the income has to be active business income. Revenue from consulting, selling products, providing services, or running operations counts. Passive investment income earned inside the corporation (interest, rental income, portfolio gains) doesn’t qualify for the small business rate.

Second, the deduction applies to the first $500,000 of that active income. Anything above $500,000 gets taxed at Ontario’s general corporate rate of 11.5%, which brings the combined federal-provincial rate to 26.5%. That’s a steep jump, and it’s worth understanding where you sit relative to that threshold.

Third, your corporation’s taxable capital needs to stay under $10 million. Between $10 million and $50 million, the Small Business Deduction phases out gradually. Above $50 million, it disappears entirely.

There’s one Ontario-specific advantage worth knowing about. Unlike the federal rules, Ontario doesn’t reduce the provincial Small Business Deduction based on passive investment income. So even if your corporation earns significant investment income inside the corporate structure, you can still access the full provincial reduced rate. That’s an advantage that doesn’t get talked about enough.

Your first year won’t be the full savings

Because the rate cut takes effect on July 1 rather than January 1, the 2026 tax year gets a blended rate. If your corporation has a December 31 fiscal year-end, the CRA requires you to prorate: the old 3.2% provincial rate applies to the first half of the year, and the new 2.2% rate applies to the second half.

That works out to an effective provincial rate of approximately 2.7% for the 2026 calendar year, which translates to a combined federal-Ontario rate of roughly 11.7%. You won’t see the full 11.2% combined rate until the 2027 tax year.

If your fiscal year-end falls on a different date, the proration split will vary depending on how many days land before and after July 1. Any corporation whose taxation year straddles the cutover date will need to track income carefully across both periods.

The dividend tax credit change that could offset your savings

This is the part of the budget that didn’t make most headlines.

Dividends paid from corporate earnings that were taxed at the small business rate are classified as “non-eligible” dividends. When shareholders receive these dividends, they get a personal tax credit called the dividend tax credit. It’s designed to offset the corporate tax already paid, and its rate is supposed to roughly align with the corporate rate.

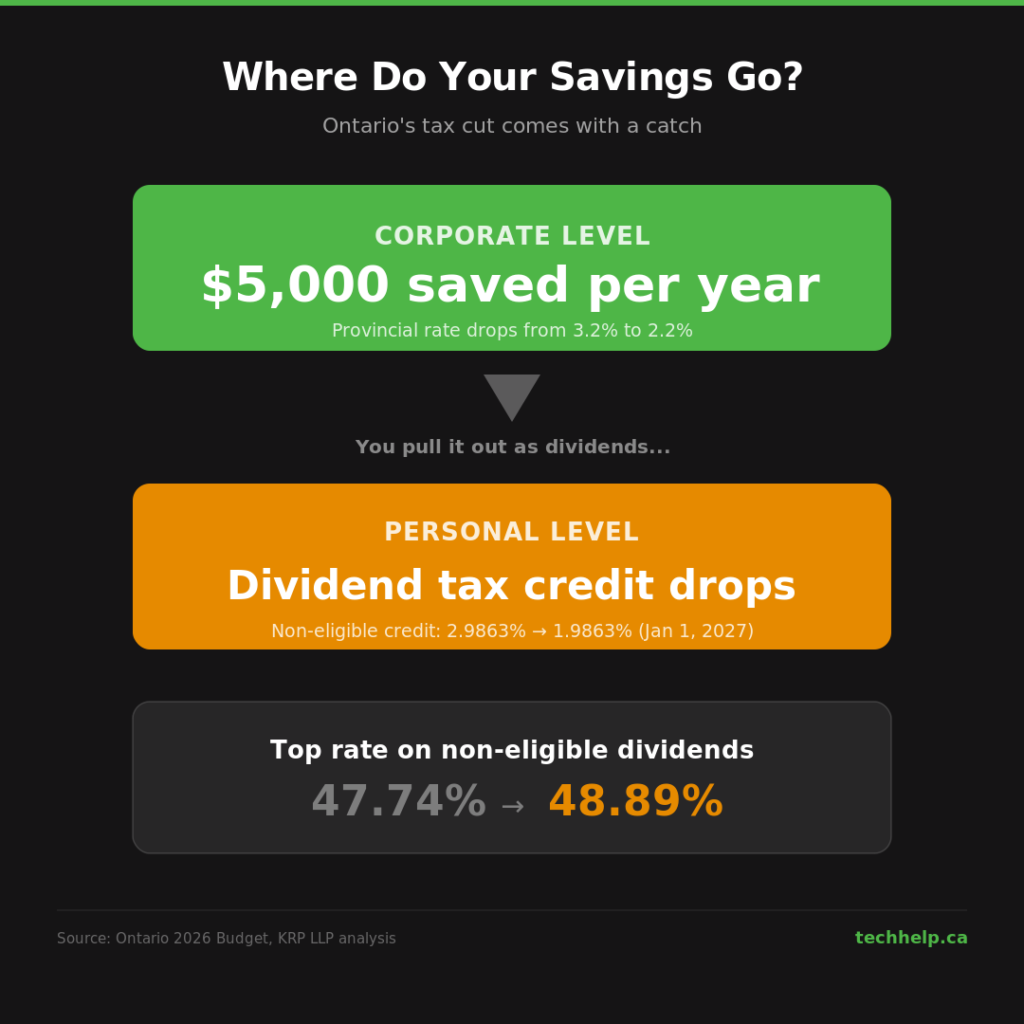

With the corporate rate dropping, Ontario is adjusting the credit to match. Effective January 1, 2027, Ontario’s non-eligible dividend tax credit rate drops from 2.9863% to 1.9863%.

In practical terms, this pushes the top personal tax rate on non-eligible dividends from 47.74% to 48.89%. For business owners who earn investment income inside their corporation, the combined corporate and personal tax rate on that income rises to approximately 58.86%, up from 57.93%.

The result is that the $5,000 you save at the corporate level doesn’t all stay saved once you pull the money out. How much gets clawed back depends on your personal income bracket and how heavily you rely on dividend distributions versus salary. For some owners, the net benefit will still be meaningful. For others, particularly those with significant retained earnings they plan to distribute as non-eligible dividends, the improvement is smaller than the headline suggests.

This doesn’t erase the benefit. But it does mean the real-world savings aren’t as straightforward as the $5,000 figure implies.

Five things to do before year-end

The gap between now and January 2027 is a planning window. Here’s where to focus.

1. Revisit your salary-versus-dividend mix

The lower corporate rate and higher personal dividend tax create a different equation for how you compensate yourself. Depending on your income level, the optimal split between salary and dividends may have shifted. This is especially relevant if you’ve been running on a strategy set years ago without revisiting it.

2. Consider accelerating non-eligible dividend payments before January 1, 2027

If you have retained earnings from income that was taxed at the small business rate, paying out dividends before the credit drops lets you lock in the higher Ontario dividend tax credit. Once 2027 hits, the same payout carries a higher personal tax cost.

3. Defer income into the second half of 2026 where possible

If you have any flexibility in when revenue is recognized, shifting income into the period after July 1 means more of it gets taxed at the new 2.2% provincial rate instead of 3.2%.

4. Track income carefully if your fiscal year straddles July 1

The CRA’s proration rules require accurate allocation of income across both rate periods. Sloppy bookkeeping here could cost you.

5. Have this conversation with your accountant now, not in December

These changes interact with passive income rules, capital thresholds, and your personal tax situation in ways that are specific to your structure. A 15-minute conversation in July is worth more than a scramble in January.

Is this enough?

The tax cut matters, and for a business earning the full $500,000 in qualifying income, $5,000 a year adds up. The CFIB’s president Dan Kelly noted that members plan to invest savings into employee compensation, expanded operations, and new hires.

But the timing of this relief matters. CFIB survey data from early 2026 shows that 72% of Ontario small businesses are being impacted by U.S. tariffs, with 28% hit directly and 44% feeling the effects indirectly. Weak demand has been the number-one barrier to growth for Ontario small businesses for 31 consecutive months. The province is also projecting a $13.8 billion deficit.

The Fraser Institute offered a different critique entirely. They argued the government cut the wrong rate. Their position: reducing the 11.5% general corporate rate would have done more to encourage small businesses to grow past the $500,000 income threshold. Right now, a business crossing that line sees its combined tax rate jump from 11.2% to 26.5%. That cliff, sometimes called the “tax wall,” can actually discourage growth. Lowering the general rate would have narrowed that gap.

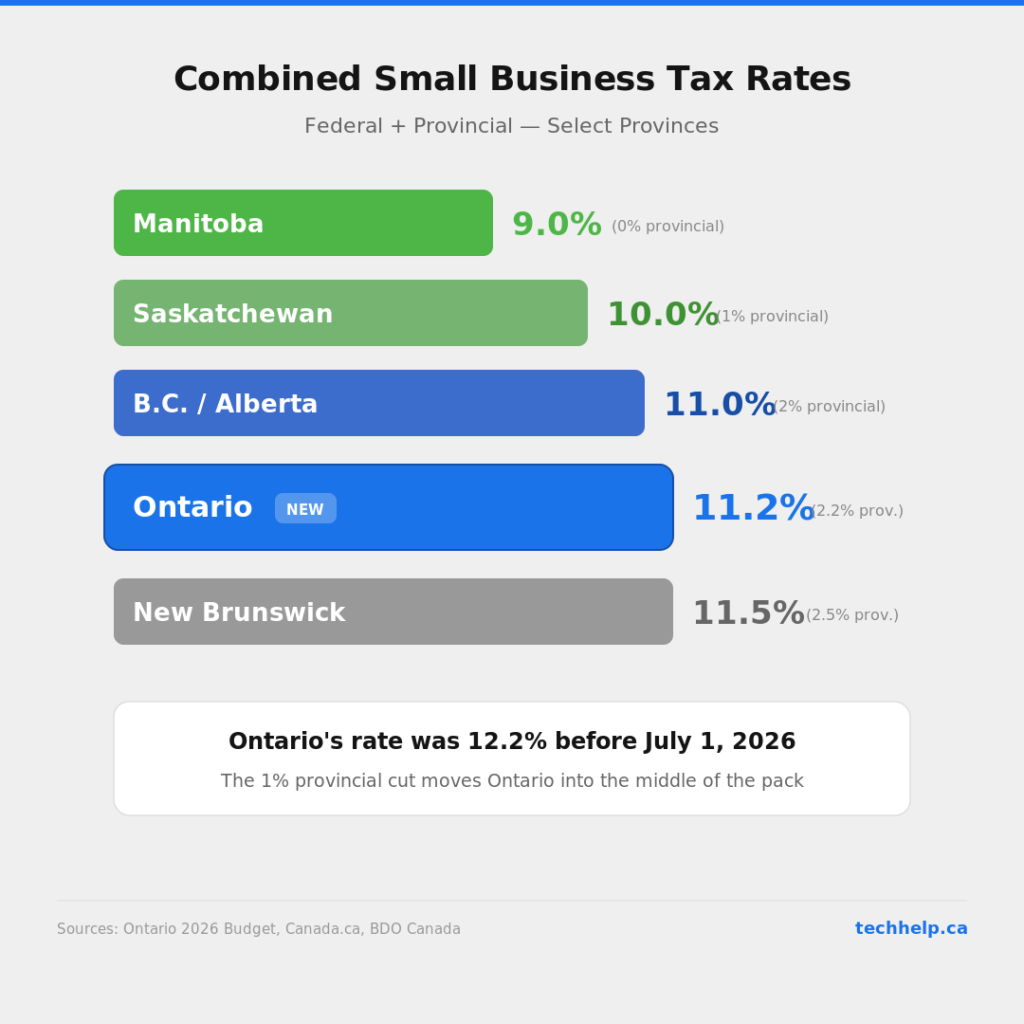

Where does Ontario land relative to other provinces? At 11.2% combined, Ontario is now close to British Columbia’s 11%. Manitoba still leads with a 0% provincial small business rate (9% combined). Provinces like New Brunswick and Newfoundland sit at 2.5% provincial rates. Ontario’s rate is competitive, but it’s not the lowest in the country.

None of this means the cut was the wrong move. It means it’s one tool in a much larger toolbox, and business owners who treat it as a windfall without understanding the dividend offset or the broader economic headwinds are likely to be disappointed.

Your move

Ontario’s small business tax cut is a genuine benefit for incorporated businesses. The savings are locked in and they’re not going away. But the paired dividend tax credit reduction, the mid-year proration, and the broader economic pressures all shape what this actually means for your bottom line.

The businesses that come out ahead will be the ones that use the next six months to plan around these changes rather than passively waiting for the savings to show up on a tax return.

This article is for informational purposes only and doesn’t constitute tax or financial advice. Consult a qualified tax professional for guidance specific to your situation.

Frequently Asked Questions

Does this tax cut apply to sole proprietors and partnerships?

No. The small business rate applies only to incorporated businesses structured as Canadian-Controlled Private Corporations (CCPCs). Sole proprietors and partnerships pay personal income tax rates on business income, so this cut doesn’t affect them directly.

What happens if my taxable capital is between $10 million and $50 million?

The Small Business Deduction phases out gradually in that range. You’ll still get a partial deduction, but the benefit shrinks as your taxable capital approaches $50 million. Above $50 million, the deduction disappears entirely and your income is taxed at Ontario’s general corporate rate of 11.5%.

Does the dividend tax credit change affect eligible dividends too?

No. Only the non-eligible dividend tax credit rate is changing. Eligible dividends, which are typically paid from income taxed at the higher general corporate rate, are unaffected by this adjustment.

Can I change my fiscal year-end to maximize savings from this cut?

Changing a fiscal year-end requires CRA approval and comes with specific rules. It’s technically possible, but it’s not something to do casually or purely for short-term tax positioning. Talk to your accountant before making any changes to your fiscal year-end.

Is this tax cut guaranteed, or could a future government reverse it?

The legislation has passed, and it’s a permanent reduction rather than a temporary measure. That said, any future government could introduce new legislation to change the rate. For planning purposes, the cut is law and in effect as of July 1, 2026.

Affiliate disclosure: Some links in this post are affiliate links. See full disclosure in the page footer.

Not sure what to read next?

I can suggest related Tech Help Canada articles based on the topic you’re reading now.

We empower people to succeed through practical business information and essential services. If you’re looking for help with SEO, copywriting, or getting your online presence set up properly, you’re in the right place. If this piece helped, feel free to share it with someone who’d get value from it. Do you need help with something? Contact Us

Want a heads-up once a week whenever a new article drops?

{kind=link}