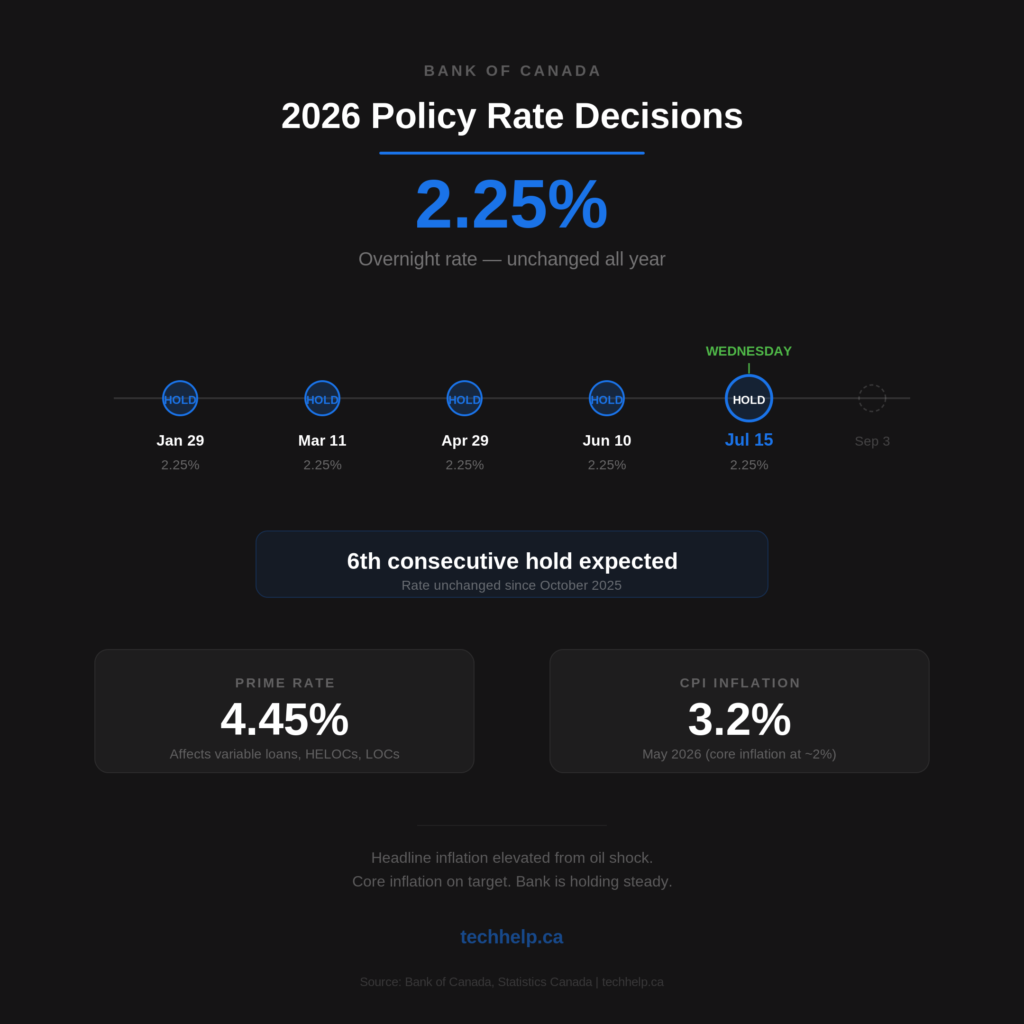

Canada’s policy rate is widely expected to stay at 2.25% on Wednesday, July 15. For business owners, the immediate effect would be straightforward: prime-linked loans and lines of credit probably won’t get cheaper this week.

The safer planning assumption is that borrowing costs remain where they are through the rest of 2026. A cut would create welcome breathing room, but building one into your budget now would leave your cash flow dependent on a decision the Bank hasn’t signalled.

Wednesday’s Monetary Policy Report will provide a better sense of what could move rates next. The Bank has to weigh weak growth against an energy-driven rise in inflation, while trade talks and household debt add risk.

The Bank of Canada will release its decision and July Monetary Policy Report at 9:45 a.m. Eastern time. Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers are scheduled to hold a press conference at about 10:45 a.m.

RBC Economics says the Bank is widely expected to hold its target for the overnight rate at 2.25%. If it does, this will be the sixth consecutive pause since the Bank’s October 2025 cut.

The decision will settle the rate for now. The report and press conference will offer more useful clues about how long the pause could last. Watch the Bank’s forecasts for growth and inflation, its assumptions about oil prices, and its language around future increases or cuts.

Why the Bank has room to hold

Inflation and growth are pulling policy in opposite directions, but neither currently makes a clear case for an immediate move.

Statistics Canada reported that the Consumer Price Index rose 3.2% year over year in May, up from 2.8% in April. Gasoline prices were 33.2% higher than a year earlier as the conflict in the Middle East and disruption through the Strait of Hormuz pushed up energy costs. Excluding gasoline, CPI rose 2.2%.

The broader inflation picture has been less alarming. At its June decision, the Bank said measures of core inflation had moved down to around 2% and that there was limited evidence of higher energy costs spreading widely across consumer prices. That gives policymakers room to look past some of the short-term jump in headline CPI.

They can’t ignore the risk of a broader increase. The Bank has said it will respond if higher energy prices start producing persistent inflation. Food purchased from stores was already 4.3% more expensive than a year earlier in May, and fuel affects shipping, travel and other operating costs.

Growth is weak enough to discourage a rate increase, but recent data also weakens the case for a cut. The economy was essentially flat in the first quarter after declining in late 2025. It then grew 0.5% in April, and Statistics Canada’s advance estimate pointed to another 0.1% increase in May. RBC Economics estimated that the second quarter was tracking toward an annualized rebound of about 2%.

That combination supports patience: headline inflation is above target, underlying inflation has been closer to it, and the economy has shown early signs of recovering from a poor first quarter.

Three signals to watch in the Monetary Policy Report

The Bank’s April report projected average GDP growth of 1.2% and average CPI inflation of 2.3% for 2026. New data has complicated both forecasts. Three parts of the July update will be especially useful for business planning.

How long the oil shock is expected to last

Oil prices have come down from their recent peak, but the Bank said in June that they were still roughly US$10 a barrel above the assumptions in its April report. The July forecast will show how quickly it expects energy-driven inflation to ease.

Cost pass-through is another key issue. The Bank’s second-quarter Business Outlook Survey found that nearly three-quarters of firms had faced higher costs because of the Middle East conflict. Among firms with those increases, roughly one-third expected to pass them on fully over the next 12 months; 25% expected to pass them on only in part, and about 40% didn’t plan to pass them on.

That split matters to the rate outlook. Broad, sustained price increases would make a future hike more likely, while businesses absorbing or only partly passing on the shock would reduce that pressure. For individual companies, absorbing costs can still squeeze margins even when it helps contain inflation.

Whether the second-quarter rebound has staying power

April’s 0.5% GDP gain marked an improvement after the first-quarter stall, with both goods-producing and service-producing industries growing. Mining, oil and gas led the increase, while manufacturing and construction also expanded.

One strong month doesn’t establish a durable recovery. The Bank’s business survey found softer sales expectations, weaker hiring intentions and ongoing spare capacity. Its new growth forecast will show whether policymakers see April as the start of firmer activity or a rebound after temporary disruptions.

How trade uncertainty affects the forecast

The United States didn’t agree to a new 16-year CUSMA extension at the July 1 joint review. The agreement remains fully in force until 2036 and can still be extended before then, but the three countries now move into annual reviews unless they agree to renew it.

For businesses, the immediate issue isn’t the agreement suddenly disappearing. It’s the uncertainty created by recurring reviews, unresolved sectoral tariffs and the possibility that companies delay orders or investment while negotiations continue. The Bank will have to account for those effects when estimating exports, investment and growth.

A hold should keep variable borrowing costs steady

Most major lenders’ prime rates are currently 4.45%. Lenders set their own prime rates, but they usually move them in step with the Bank’s policy rate. If the Bank holds and lenders follow their usual practice, prime should remain at 4.45%.

That would leave the rate unchanged on many variable-rate mortgages, home equity lines of credit, personal lines of credit and variable-rate business loans. Your actual rate may be quoted as prime plus or minus a set amount, so the contract determines what you pay.

Some variable mortgages have payments that adjust when prime changes. Others keep the payment fixed and change how much goes toward interest and principal. Both structures should keep their current interest rate after a hold, but they’ll respond differently when prime eventually moves.

RBC Economics expects the Bank to remain on hold through 2026. That’s one forecast, not a commitment from the Bank. Oil prices, trade policy, inflation and growth can change the path before year-end.

Fixed borrowing costs can move without the Bank

Fixed mortgage rates respond more to Government of Canada bond yields than to the overnight rate. They can rise or fall between Bank announcements as investors reassess inflation, growth and global risk.

Ratehub’s advertised high-ratio five-year rates on July 13 started at 3.94% fixed and 3.45% variable. Those are starting rates for borrowers who meet specific conditions, not universal offers. Renewal, refinance and uninsured rates may be higher, and the quote available to you can depend on equity, credit, property use, province and lender.

The gap between those two advertised rates was 0.49 percentage points. The lower variable rate comes with the risk that payments or interest costs rise later. A fixed rate buys payment certainty, but it can come with different prepayment penalties, portability rules and refinancing costs.

Compare those contract terms alongside the rate. A slightly cheaper loan can become the more expensive option if you expect to sell, refinance or repay early.

Mortgage renewals can reach the business in two ways

The Bank of Canada’s 2026 Financial Stability Report says the final group of five-year, fixed-payment mortgages taken out at very low pandemic-era rates will renew over the next 12 months. These loans represent about 12% of outstanding mortgages, and the Bank expects payments to rise by about 15% on average.

Most households that have already renewed at higher rates have managed the increase, and mortgage arrears remain low overall. The pressure is uneven. CMHC expects arrears to keep rising moderately through late 2026, with Toronto facing the strongest increase and Vancouver also showing added strain.

If you own a business and a home, a larger mortgage payment can reduce the personal cash available to support the company or cover an uneven month. Keep the household renewal in the same planning conversation as business debt, especially if you’ve signed a personal guarantee.

Your customers may also be renewing. A 15% average payment increase won’t affect every household, and some borrowers are extending amortizations to limit the monthly jump. Businesses that depend on discretionary consumer spending should still watch average order value, delayed purchases and demand in regions with heavier mortgage stress.

Use the pause to test your borrowing plan

A hold gives you a stable starting point. Use it to find out whether a quarter-point increase would create a manageable expense or a cash-flow problem.

Map every prime-linked balance

List each variable-rate loan, line of credit, HELOC and financing agreement. Record the balance, current rate, prime adjustment, payment structure, renewal date, maturity date and any personal guarantee.

Check which facilities reprice automatically and which allow the lender to change the spread. The words “variable rate” don’t tell you enough to model the cost accurately.

Price a quarter-point increase

As a rough first calculation, a 0.25-percentage-point increase adds $1,250 a year in interest to a constant $500,000 balance. Amortization, changing balances, fees and payment rules will affect the amount you actually pay, so use your lender’s figures for the final forecast.

Run two 12-month cases: one with prime holding at 4.45%, and another with prime rising to 4.70%. Keep a possible cut out of the base case. If the higher scenario strains payroll, inventory purchases or tax payments, you have a financing issue to address before rates move.

Compare flexibility before converting debt

Don’t choose fixed or variable financing from the headline rate alone. Ask for the conversion rules, prepayment formula, portability terms, renewal options and total cost in writing. For business debt, check whether changing the rate structure also changes covenants, security or guarantees.

Certainty may be worth paying for when margins are thin and a higher payment would force cuts elsewhere. Flexibility may be worth more when you expect to refinance, sell an asset or repay the loan early. Your lender, accountant or mortgage professional can price those trade-offs using your contract and tax position.

Watch customers as closely as your loans

Higher fuel costs and mortgage renewals can reduce what customers have left for optional purchases. Track changes in order size, payment timing, financing use and cancellations rather than waiting for a broad economic indicator to confirm what your sales data already shows.

If demand is softening, protect cash before committing to new fixed expenses. If your sales remain steady, you can make decisions from your own evidence instead of assuming every national warning applies equally to your market.

Plan from today’s rate, not tomorrow’s hope

Wednesday’s likely hold should keep prime-linked borrowing costs stable. The July report may change expectations about how long that stability lasts, but it won’t make a future cut certain.

Before the announcement, put 4.45% and 4.70% prime into your next 12-month forecast. If the higher case breaks the plan, talk to your lender while rates are still flat. A pause gives you time to prepare before the next move changes the math.

Affiliate disclosure: Some links in this post are affiliate links. See full disclosure in the page footer.

Not sure what to read next?

I can suggest related Tech Help Canada articles based on the topic you’re reading now.

We empower people to succeed through practical business information and essential services. If you’re looking for help with SEO, copywriting, or getting your online presence set up properly, you’re in the right place. If this piece helped, feel free to share it with someone who’d get value from it. Do you need help with something? Contact Us

Want a heads-up once a week whenever a new article drops?

")

")

{kind=link}